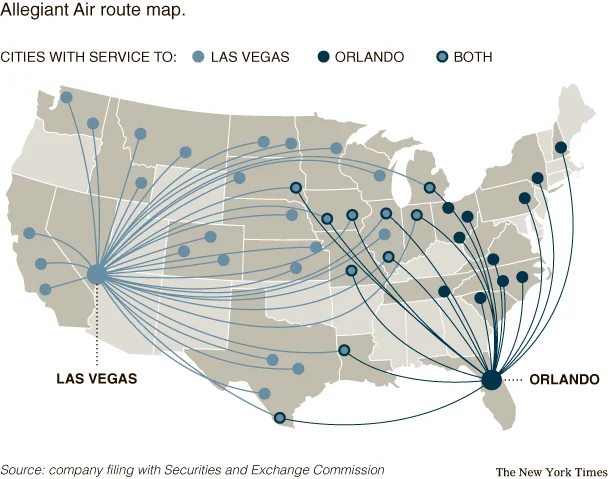

Allegiant Airlines Passenger Growth: What the 12.6% Surge Actually Means

More Passengers, Less Full Planes: Deconstructing Allegiant's Growth Paradox

At first glance, news that Allegiant airlines posts 12.6% passenger surge August - Rolling Out reads like a victory lap. The Las Vegas-based budget carrier announced it flew nearly 1.5 million people, a significant jump from the previous year. Passenger numbers were up by over 12%—to be more exact, 12.6%. Revenue passenger miles, a key measure of demand, climbed a healthy 12.1%. The executives are, predictably, bullish. CFO Robert Neal points to manageable fuel costs and strong operational performance, while CCO Drew Wells touts booking trends that are "outperforming expectations."

On the surface, it’s a simple, compelling story of growth. The airline is flying more planes and carrying more people. The market loves a growth story.

But when you peel back the first layer of data, a more complex and far more interesting narrative emerges. The numbers don't just tell a story of growth; they reveal a deliberate and risky strategic choice. The core of it lies not in the numbers that went up, but in the one crucial metric that went down: the load factor. It slipped from 84.5% to 82.6%. While a 1.9 percentage point drop might seem trivial, in an industry of razor-thin margins, it’s a flashing yellow light. It tells us that while Allegiant’s planes carried more people in total, the average plane was less full than it was a year ago.

And that begs the real question: Why?

The Widening Gap Between Capacity and Demand

To understand what’s happening, we have to look past the headline passenger count and examine the two metrics that truly define an airline's operational balance: Available Seat Miles (ASM) and Revenue Passenger Miles (RPM). Think of ASM as the airline's total inventory—every seat on every plane, multiplied by the distance flown. It’s a measure of capacity. RPM, on the other hand, is the inventory that was actually sold (a metric that essentially measures the total distance traveled by paying customers).

Here is the discrepancy. While demand (RPM) grew by a respectable 12.1%, Allegiant’s capacity (ASM) grew by a much larger 14.6%.

This isn't an accident. It’s a conscious decision. The airline increased its total number of departures by a staggering 15.9%. They put more planes in the air, flying more routes, and added seats to their network at a pace that outstripped their ability to fill them with paying passengers. This is the mathematical source of the declining load factor.

It’s like a restaurant owner who, encouraged by a steady increase in customers, decides to build a massive new 100-seat extension. The next month, they proudly announce they served 10% more diners. But what they don't highlight is that to achieve that, they had to increase their total seating by 25%, and now the new extension sits half-empty every night. The restaurant is technically bigger and serves more people, but it has become less efficient. The core business is less profitable on a per-unit basis.

This is precisely the scenario reflected in Allegiant’s August data. So, is this a strategic blunder or a calculated risk?

A Calculated Gamble on Future Dominance

I’ve looked at hundreds of these filings, and this is a classic move for a company in an aggressive expansion phase. My analysis suggests Allegiant is deliberately trading short-term efficiency for a long-term strategic footprint. The airline's entire model is built on connecting smaller, underserved cities to leisure destinations, avoiding direct combat with the legacy carriers. This rapid increase in departures and capacity signals a potential "land grab"—an effort to lock down new, profitable niche routes before a competitor can.

They are willing to fly slightly emptier planes today to own a market tomorrow.

The commentary from the C-suite provides the context for this gamble. When CFO Robert Neal mentions that fuel costs are stable and non-fuel operational costs are "performing better than anticipated," he’s not just offering a rosy update. He’s signaling that the company has the financial cushion to absorb the inefficiency. Lower costs per flight mean they can tolerate a lower load factor without cratering their margins. They can afford, for now, to operate those less-full planes. It’s a calculated bet, backed by a favorable cost environment.

But this strategy invites critical questions that the press release doesn't answer. How long is this trade-off sustainable? At what point does a declining load factor begin to erode the very operating margins the company expects to hit the "higher end" of its forecast? And while "strong" booking trends for the fall sound promising, will that new demand be strong enough to close the 2.5-point gap between capacity growth and demand growth? Or will it just keep pace, leaving the efficiency problem unsolved?

The data shows us what Allegiant is doing. The executive commentary tells us why they think they can get away with it. What remains completely unknown is whether the gamble will actually pay off.

Efficiency Is a Choice, Not a Given

Ultimately, Allegrant's August report isn't a story about simple growth; it's a story about a conscious strategic choice. The airline is choosing expansion over optimization. They are betting that securing new routes and markets now will yield greater returns down the road, and they believe their cost structure is strong enough to weather the temporary inefficiency. It's a bold, aggressive posture. The problem with any bet, however, is that it can be lost. The coming quarters will reveal whether this expansion was a visionary move to build a wider moat or a costly overreach that sacrificed the discipline that made the airline successful in the first place.

Related Articles

Powell's Speech: Decoding the Market Impact and Future Rate Cuts

All eyes are on Washington, D.C. tomorrow. Not on Congress, not on the White House, but on a single...

Federal Solar Incentives Are Ending: A Data-Driven Breakdown of the Financial Impact

Oregon Governor Tina Kotek is in a race against the clock. With an executive order, she has directed...

Hims Stock Surges 39%: A Data-Driven Look at the Surge

The ticker for Hims & Hers Health (HIMS) has been on a tear. A 39% surge in a single month is the ki...

GMA's Deals and Steals: A Surprising Glimpse into the Future of Retail

I want you to look past the popcorn tins and the splatter guards for a moment. On October 11th, a se...

Netflix Stock Price: A Ten-for-One Split... Really?

Netflix's 10-for-1 Split: Don't Fall for the Hype Alright, so Netflix is doing a 10-for-1 stock spli...

Dow Futures Dive: Rate Cut Doubts Deepen

US stocks took a dive on Friday, extending a week of losses that’s got everyone from retail investor...